Understanding tax residency

Changing your tax residency does not affect your citizenship status, but it does affect how much money you owe SARS.

South Africa has a residency-based tax system, which means that tax residents are taxed differently from those who are no longer considered resident in the country.

- If you are a tax resident and live in South Africa, you must pay SARS tax on all worldwide income.

- If you are a tax resident, but live and work overseas for most of the year*, you do not need to pay SARS tax on your worldwide income and the first R1.25 million of employment income is not taxed. Income earned over and above that amount will still be taxed in South Africa.

- If you are not a tax resident, you only have to pay SARS tax on the income you earn in South Africa (e.g. from renting out a South African property or dividends from a South African company).

*Longer than 183 full days in any 12-month period (with at least 60 of those days being consecutive)

If you are tax resident in South Africa, Double Taxation Agreements (DTAs) between countries can protect you from having to pay tax on your foreign income in both South Africa and another country or allow you to pay a reduced rate. It’s worthwhile looking into the DTAs in place between South Africa and your new country of residence to ensure you’re not paying too much tax.

We offer specialist, personalised, end-to-end accounting and tax advice

How SARS determines your tax status

SARS conducts two "tests" to consider whether you should be deemed tax resident.

The Ordinarily Resident test

This is a subjective test that seeks to determine where your main home is.

SARS will look at factors like:

- Where your family lives

- Where your permanent home is

- If you have belongings in storage in South Africa

- If you regularly return to a place in South Africa

The Physical Presence test

If SARS decides you are ordinarily resident outside of South Africa, it will conduct a second test. This looks at the number of days you spend out of the country.

To prove non-resident status, you need to avoid being in South Africa for a period exceeding:

- 91 days in total during the tax year under consideration

- 91 days in total during each of the five tax years preceding the one under consideration

- 915 days in aggregate during the above five preceding tax years – which amounts to an average of 183 days a year.

How can I change my tax residency status?

Tax emigration should be reported in the tax return covering the period you alter your status. If you failed to report it at the time, you can back date it but may face penalties and have to pay Capital Gains Tax (CGT) on your current asset base.

We offer specialist, personalised, end-to-end accounting and tax advice

Exit tax when you leave South Africa

Capital Gains Tax (CGT) is a tax you pay whenever you make a profit from selling something you own. When you declare yourself non-tax resident, you’re deemed to have sold your assets (excluding immovable property situated in South Africa and your RA) to your foreign self. A CGT amount, known colloquially as “exit tax”, then becomes immediately due.

In South Africa, CGT is not a flat rate. A portion gets added to your other income for that tax year and you’re taxed in your tax bracket. The CGT rate can range from 7.2% to 18% depending on the tax bracket you’re in. If you leave South Africa early in the tax year, your total income for the tax year is lower and therefore the CGT may be lower than when you’re settled in your new home. This is one reason it’s better to tax emigrate sooner rather than later.

However, there are a range of complex factors that can influence how much you pay and when. We recommend seeking professional advice before attempting to alter your tax status. We are South African tax emigration specialists who can assist in managing the entire process from end-to-end.

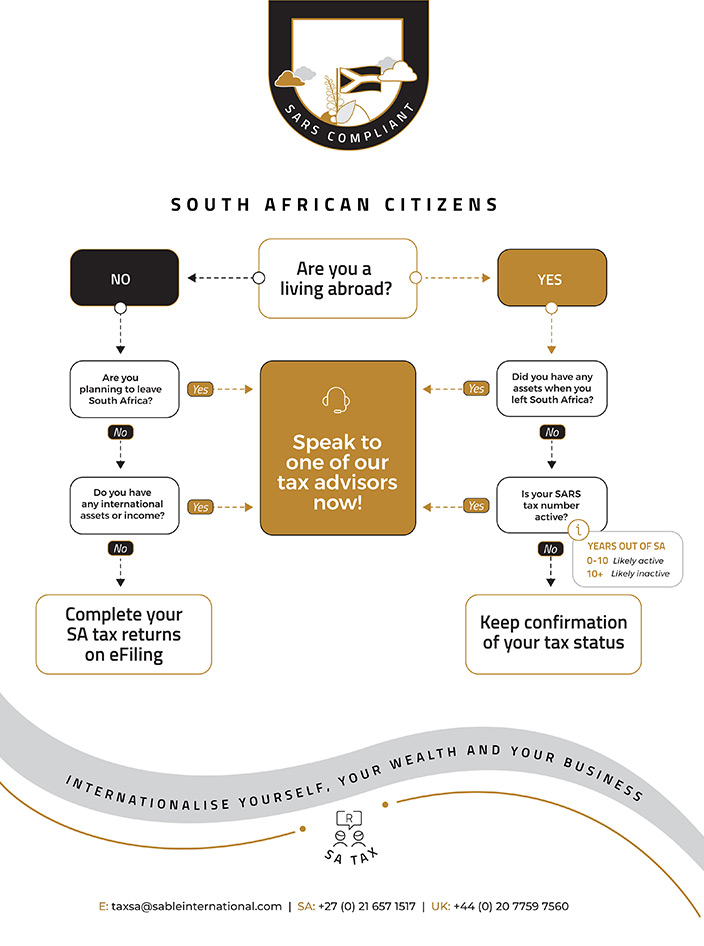

Do you have to file a tax return in SA?

Get in touch

Fill in your details below and one of our consultants will be in touch as soon as they are able.

Cyber Essentials

Our Cyber Essentials certification reflects our ongoing commitment to cybersecurity best practices, ensuring that we safeguard sensitive data and operate with a high level of digital integrity.

Considering returning to SA?

Book a complimentary consultation now with our experts - we can help you with everything from wealth and tax to foreign exchange transfers, to ensure a smooth financial transition.

Book a complimentary consultation