Sable Wealth Investment Committee Report: Schrodinger’s Recession

Sable Wealth’s Investment Committee offers an overview of the factors impacting financial planning from 2023 into 2024.

Staff Writer ● Sep 18, 2023

Staff Writer ● Sep 18, 2023

The year so far has been one of watching and waiting as we try to assess where we are in one of the largest economic transition periods since the war.

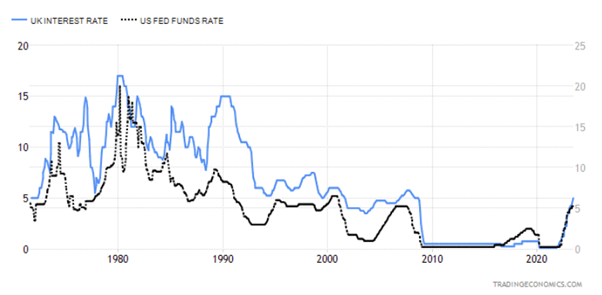

2022 was a watershed moment for the global financial system. The sudden arrival of significant and severe inflation signalled the end of 30 years of falling interest rates. The graph below shows how following the financial crisis in 2008/09 interest rates effectively fell to zero and stayed close to zero until the inflation shock of 2022 arrived.

Source: Tradingeconomics.com

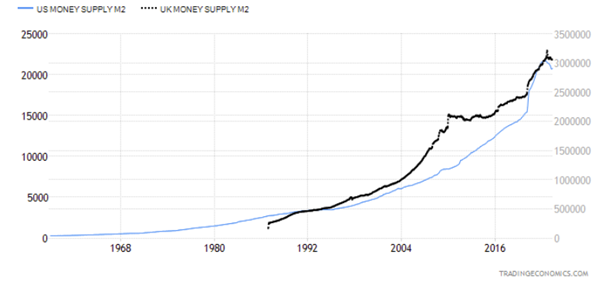

Low interest rates were accompanied by all monetary stimulus (QE) resulting in the largest expansion of the global money supply in history. The chart below shows the M2 (broad) measure of money supply for the US and the UK.

Source: Tradingeconomics.com

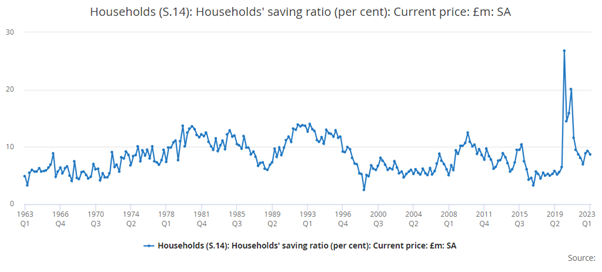

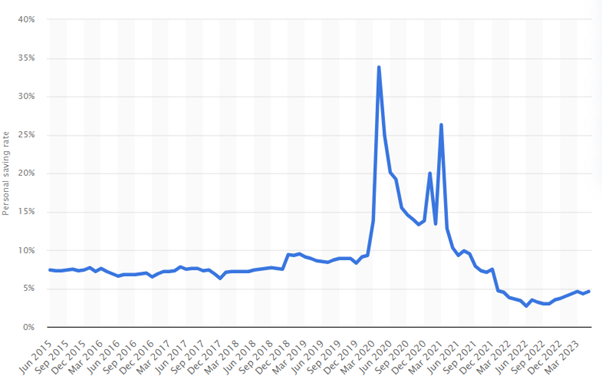

By late 2020, some market participants were speculating that the post-financial-crisis stimulus, when added to the Covid stimulus, would not cause an inevitable rise in inflation. Central banks clung to a narrative of ‘transitory inflation’, believing the Covid restart was the primary inflationary force. The Ukraine war then provided the supply side shock needed to trigger a bigger inflationary spike as energy costs fed into the wider inflationary environment. Furthermore, household savings peaked during Covid to all-time highs, further stocking the building inflation storm. Below are two graphs showing the UK and US household savings:

Source: Office of National statistics

Source: Statista

By the end of 2022, bond prices had fallen (and yields risen) sharply. The UK had experienced a bond market crisis set off by the disastrous August budget and equity valuations had receded. In one short half year, a 30 + year trend in global macroeconomics had suddenly reversed. The impact on asset classes was for long bond portfolios to experience severe downturns while growth equities fell in tandem.

See also: Don’t sell the bonds in your portfolio

Late 2023 – where to now?

Our current macro-economic situation reminds me of Schrodinger’s Cat. Are we dead or are we not dead?

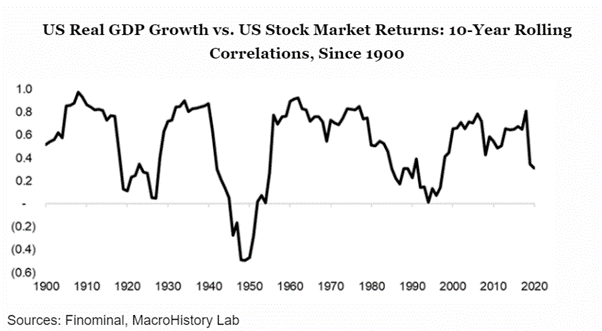

It’s a case of the recession that never arrives. That is possibly explained by the personal savings graphs above. Our view is a hard landing in the UK looks unavoidable due to the unique nature of the supply chain and labour market challenges created by Brexit and the energy price shock, all made worse by the self-harm of the Truss Budget in August 2022. A soft landing in the US and Euroland is possible but optimistic. A highly likely scenario is what BlackRock calls "full employment stagnation", a form of economic stagnation where the economy still experiences rising wages due to mismatch in skills between sectors while employment is almost full. It’s a new and specific form of ‘secular stagnation’ (i.e. rising prices at the same time as falling growth). Indeed, BlackRock also comments that the post-Covid period has seen a large shift in consumer spending patterns from services outside the home to goods inside the home and this switch has created the skills mismatches playing out in labour data. That said , it is important to remember that the economy and the stock market are different phenomena that respond to different stimuli. The graph below shows how the correlations between the stock market and Real GDP growth have broken down over time.

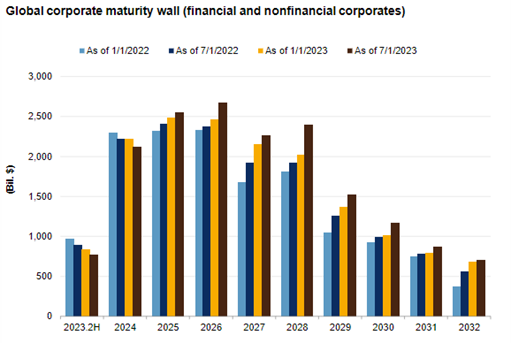

The price of the stock market, of course, reflects the forward-looking expected returns of owners of capital. GDP reflects the overall activity of the overall economy, which includes labour and governments. The point is, economic predictions can be misleading for investors when there is an economic regime change such as we are seeing now in the change in power relationships between capital, labour and governments. The marked change in the cost of capital, along with the reduced supply of low-cost labour, changes profitability outlooks in different sectors. While credit supply is receding, the stock of corporate debt in issue now still needs to be refinanced. As this stock gets refinanced, we will see corporate earnings affected by more than the cost of the new debt. The graph below shows the maturity wall approaching.

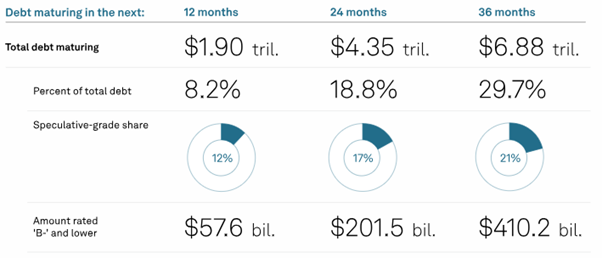

Importantly, the more of the near-term debt is investment grade, the bulk of the lower grade (speculative) debt follows:

Therefore, the impact of higher interest rates is yet to be fully felt in the corporate sector, but that impact is approaching and the impact on the debt for lower-rated corporates should arrive in full by 2026.

So timing is everything?

With the backdrop above, it’s understandable (almost) that we’ve seen periods of very unusual pricing in asset markets. Below is a chart from July this year showing the earnings yield of the S&P, the corporate bond yield and the cash yield – all converging around 5.5% as illustrated in the chart below from M&G’s Bond Vigilantes.

You might well ask why a market would willingly price the equity yield, bond yield and cash yield at the same level. At a glance it would suggest equity prices are elevated, bond prices are depressed and/or cash returns are wildly elevated.

What we are seeing is a wide dispersion in views on near-term path for inflation and, therefore, interest rates and what that analysis leaves as conclusions for the impact of the refinancing cycle. In short, if global inflation falls quickly, and interest rates follow, the refinancing cycle impact on lower-grade corporates may be muted and thus economic scarring reduced – read ‘soft landing’. If inflation persists and settles in at around 5%, the refinancing realities will yield casualties – read ‘hard(er) landing’. We don’t have a crystal ball and today’s pricing shows that no-one else does either!

See also: 10 attributes of great financial advisers

In these unprecedented times, it’s more important than ever to carefully consider your investment strategy and the risks. Speak to us about financial planning to see how we can create the right solution for your needs. Email [email protected] or give us a call on +27 (0) 21 657 1540 (SA) or +44 (0) 20 7759 7519 (UK).

Sable Private Wealth Management Limited is authorised and regulated by the FCA (no. 222501). Sable Private Wealth (Pty) Ltd is authorised by the FSCA (no. 48122).

Cyber Essentials

Our Cyber Essentials certification reflects our ongoing commitment to cybersecurity best practices, ensuring that we safeguard sensitive data and operate with a high level of digital integrity.